Internet tips for jewelry insurers

We know consumers turn to the internet to shop for jewelry, but have you thought about how the ‘net is also a useful tool for jewelry insurers?

We know consumers turn to the internet to shop for jewelry, but have you thought about how the ‘net is also a useful tool for jewelry insurers?

Suppose you have a submission before you, and you’re wondering ...

Is the valuation realistic?

As we’ve discussed in earlier issues, grossly inflated valuations are extremely common. Online purchases and jewelry bought on vacation are particularly suspect.

If you are suspicious, try checking the site Blue Nile. Using the “build your own ring” feature, you can enter the specific characteristics of the diamond and setting, as given on the appraisal. A picture of the ring and a price will appear. This site’s price is somewhat lower than a brick-and-mortar jewelry store would charge, because of the volume of business Blue Nile does, but the price is a figure to work with.

How about the valuation of a vintage Rolex?

How about the valuation of a vintage Rolex?

Insurers often receive appraisals for old Rolexes with valuations that match the MSRP of the current model. Such outrageous valuations should not be accepted.

A luxury watch is a quality machine but watch parts, such as mechanisms and bracelets, wear out. With the exception of rare collector pieces, watches begin losing value as soon as they walk out the door, just as cars decline in value the minute they drive off the lot.

A good site to check is Bobs Watches, which buys and sells luxury vintage watches, especially Rolexes. The site lists both the customer’s Buy price and Sell price. The Buy price is a good indication of an appropriate valuation for the watch.

Caution: Keep in mind that there is a huge market in counterfeit Rolexes, and Rolex considers watches that contain any non-Rolex parts to be counterfeits. Adjusters should be sure the insured watch was an authentic Rolex before replacing with an authentic Rolex. See these earlier issues of JII for some of the risks involved with insuring Rolexes: risks 1-4 risks 5-7 risks 8-10 risks 11-12

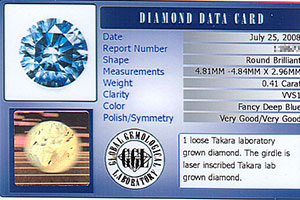

How significant is the brand name shown on the docs?

![]()

![]()

![]()

A brand name could carry important information about valuation.

The name may be the manufacturer of lab-created gems (e.g., Chatham), info that will be proudly stated on the company’s website. Or the name could identify a clarity enhancement (e.g., Yehuda) that makes fractures in the stone less visible to the unaided eye. Or it might be a company that sells the diamond look-alike Moissanite (e.g., Charles & Colvard).

Reputable companies are up-front about their products on their websites. It is important for insurers — especially in settling a claim — to know that the values for gems that are lab-grown, enhanced, or simulant diamonds, are not comparable to the prices of untreated mined diamonds.

Sometimes, though, a brand name is just a name. For further discussion, see Is that brand-name diamond really a cut above? and Tiffany v. Costco .

What is the insured’s occupation?

Many insurers decline coverage for jewelry owned by professional athletes or entertainers because of the high risk of damage or loss. Sometimes the insured’s listed occupation is a little vague. Is an “event planner” planning wedding receptions or rave parties? Is a photographer doing fashion shots in his studio or covering battles in the world’s current hot spot?

Simply entering the insured’s name or his company’s name in the search bar can sometimes give you the information you need.

Is the diamond cert legit?

Pretty much every piece of jewelry comes with some “certificate” these days. There are dozens of labs producing such documents, which might be called Lab Report, Grading Report, Certificate of Authenticity, Gem I D Card, Diamond Data Card, or any number of other names.

Some labs are known for their exaggerated grading; some merely repeat the seller’s description of the jewelry; and some “labs” are completely bogus, with no street address or web presence.

To be of value, the lab report must come from a lab that is independent of the seller and has a reputation for accurate grading. We recommend the following reliable labs. If the submission includes a report from one of these labs, or if a report number is mentioned on the appraisal, you can easily verify it online by using these links:

GIA Report Check

AGS Report Verification

GCAL Certificate Search

When you enter the report number, you’ll see the basic report information. Check that the 4 C’s in the report agree with what you see in the appraisal to be sure the lab report is for the gem you are insuring.

FOR AGENTS & UNDERWRITERS

These are just a few tips to remind you of an easily accessible resource.

FOR ADJUSTERS

If there are any terms on the appraisal that you don’t understand, try looking them up online. It could give you information about quality and value.

©2000-2025, JCRS Inland Marine Solutions, Inc. All Rights Reserved. www.jcrs.com

Subscribe to Jewelry Insurance Issues