Valued Contract for Jewelry? —

Proceed with Caution!

Most valued contracts on jewelry are magnets for moral hazard. Why? Because jewelry’s scheduled value is often well above its actual cash value, and may even be well above its purchase price.

A few examples:

Example 1

The

web site for Sam’s Club, a division of Wal-Mart, advertised a ring for

$260,000. To prove the price was a bargain, the site also showed an appraisal

valuing the ring at $450,000, almost twice the selling price.

The

web site for Sam’s Club, a division of Wal-Mart, advertised a ring for

$260,000. To prove the price was a bargain, the site also showed an appraisal

valuing the ring at $450,000, almost twice the selling price.

Wal-Mart is the nation’s largest jewelry retailer, selling more than $2.5 billion per year. And they do sell high-end jewelry.

Example 2

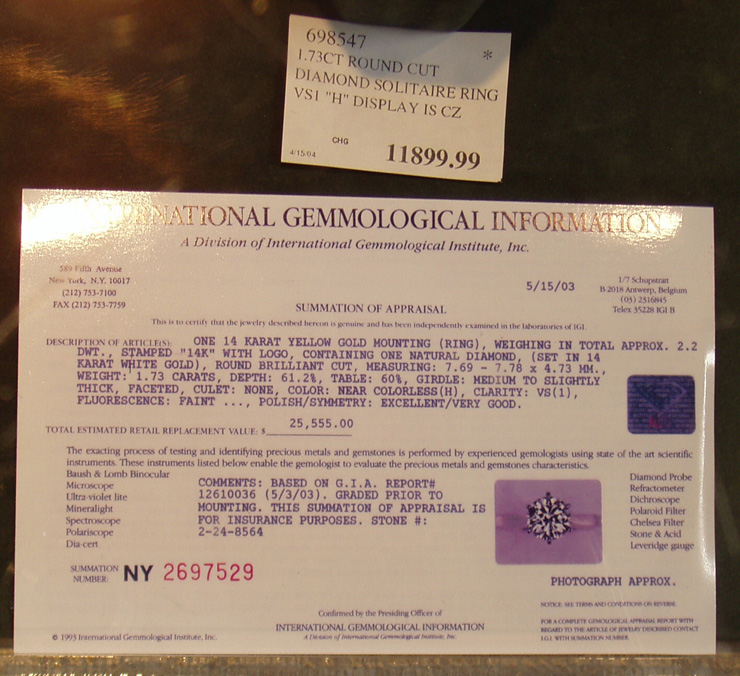

Nor are such excesses limited to the Internet. Here’s a retailer’s display case showing appraisals right next to the jewelry. In all instances, the appraised value is about twice the selling price.

Click the picture to see one of the appraisals

close up.

Just a few weeks ago NBC’s Dateline alerted the public to the widespread use of inflated appraisals to lure customers. Their investigators went to several stores and bought diamond rings selling at prices well below their appraisal valuations. To see a video clip of their report “Diamonds: Is There Such a Thing as a ‘Deal’?” follow this link: https://www.msnbc.msn.com/id/8661995/

Such inflated “appraisals” are actually sales tools. The retailer supplies them to make the buyer feel good about the purchase. Not that the buyer is being cheated. JCRS has found that, in many cases, the selling price reflects competitive retail value. It’s the appraisal that is grossly inflated. But too often such appraisals make their way into the insurer’s files.

If the insurer wrote a valued contract based on any of those appraisals:

- the insured might be tempted to “lose” the jewelry and “win” a settlement

- any claim, whether real or fraudulent, would result in vast overpayment.

You might think that people who have expensive jewelry also have a lot of money and therefore wouldn’t be tempted to file a fraudulent claim. However, a survey by Accenture found that 25% of consumers — regardless of their economic station — feel it is OK to file inflated or non-existent claims. Companies that write valued contracts have built such fraud into their rates.

Example 3

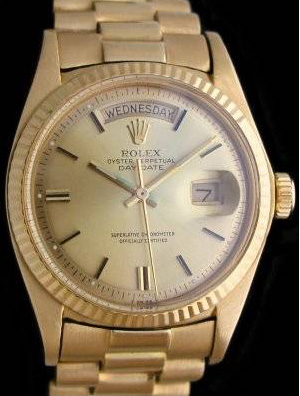

A

25-year-old men’s Rolex has a suggested list price of $20,000. Yet that

identical 25-year-old watch can be replaced for about $6,000-$8,000. Why would

this watch be written under a valued contract? A settlement should put the

individual in the same position as before the loss occurred, not make him

richer.

A

25-year-old men’s Rolex has a suggested list price of $20,000. Yet that

identical 25-year-old watch can be replaced for about $6,000-$8,000. Why would

this watch be written under a valued contract? A settlement should put the

individual in the same position as before the loss occurred, not make him

richer.

Actual Cash Value (ACV)

In the vast majority of cases, jewelry is best written on a standard ACV form. Actual Cash Value is determined at time of loss. Settlement is based on the cost to repair or replace the jewelry article with one of like kind.

Referring to Example 3 above, this means the insurer could replace the Rolex with one of the same vintage for $6,000-$8,000, rather than paying out $20,000. (Obviously, the difference between a new watch and a 25-year-old watch is depreciation.)

Actual cash value also eliminates the hazard of inflated appraisals. An insurance policy is not a vehicle for profit.

Policyholders sometimes argue that, since they are paying premiums based on their jewelry’s appraisal, they are entitled to a settlement equal to that amount. They must understand that the ACV policy requires the insurer to determine value at time of loss. (This could be higher or lower than the appraised value, but the insurer does not pay more than the limit of liability.)

Here’s another way to think about it. If we started offering replacement cost and valued contracts on autos, people would be conveniently finding telephone poles to back into, or they would set their cars up to be stolen. With cars, insurers have a lot of statistics, so we know a valued contract doesn’t make sense.

With jewelry, we have no real loss statistics. Most insurers maintain statistics only on scheduled personal property, which includes jewelry right along with computers, cameras, fine arts, etc. All those other classes are far less hazardous to loss than jewelry. They are, in effect, subsidizing jewelry.

Agents might also consider how their profit-sharing/contingency agreements are affected by overly generous settlements. How many premium dollars are needed to offset one excessive payout?

As noted in our July issue, almost all jewelry can be duplicated. ACV policy terms allow the insurer to have a duplicate made, thus returning the insured to the same position as before the loss. Replacing lost or damaged jewelry (or offering the cash equivalent of the cost to repair or replace) is normally much less expensive than paying the total amount under a valued contract.

The RARE Occasion

A valued contract IS called for when a piece of jewelry is truly irreplaceable, in which case there must be agreement. As discussed in our July issue, unique and irreplaceable jewelry is extremely rare. In most cases, actual cash value (ACV) is the reasonable, fair and cost-effective solution.

If a valued contract is to be used, at least it should be based not on inflated values but on a reputable insurance-to-value calculation.

FOR AGENTS & UNDERWRITERS

Score the appraisal, using the Jewelry Appraisal and Claim Evaluation form (ACORD 18).

If the appraisal lacks crucial information, encourage the policyholder to submit the insurance industry’s standard Jewelry Appraisal (ACORD 78/79), written by a Certified Insurance Appraiser™.

Perform ITV (insurance-to-value) calculations, for which software is available.

Ask for the sales receipt, as well as an appraisal. If it is a recent purchase, we suggest, in most cases, that you not insure the jewelry for more than 125% of its purchase price.

FOR ADJUSTERS

In settling a valued contract, your only option for reducing losses is to encourage the client to take replacement in lieu of a cost settlement.

If the jewelry was purchased within the past year and the price is significantly less than the appraisal, be suspicious of fraud and consider involving your SIU (special investigative unit).

Typical language on standard ACV form for covering

jewelry

(“other property”):

| 1. | The value of the property insured is not agreed upon but will be ascertained at the time of loss or damage. We will not pay more than the least of the following amounts: | |

| a. | the Actual Cash Value of the property at the time of loss or damage; | |

| b. | the amount for which the property could reasonably be expected to be repaired to its condition immediately prior to loss; | |

| c. | the amount for which the article could reasonably be expected to be replaced with one substantially similar to the article lost or damaged; or | |

| d. | the amount of insurance. | |

©2000-2025, JCRS Inland Marine Solutions, Inc. All Rights Reserved. www.jcrs.com

Subscribe to Jewelry Insurance Issues