What Is A Good Appraisal?

Which of these are good appraisals?

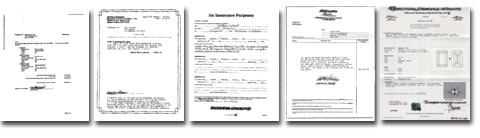

Click each appraisal to see an enlargement

Was that a trick question? Yes.

The answer is: NONE of them.

And that usually leads to settlement overpayments.

Let's have a closer look. These are real-world appraisals, typical of those received every day by agents and underwriters and used by adjusters to settle claims. We scored them for completeness using ACORD 18, Jewelry Appraisal & Claim Evaluation.

Yellow highlighting shows missing information that is crucial to accurate valuation. (Click on a graphic to view a full-sized form in a new window. Close the new window to return to the story.)

Appraisal 1

|

|

Appraisal 1 |

Appraisal 1 |

The orderly presentation of information is misleading. This appraisal doesn't

discuss mounting at all, and doesn't even say what metal is used.

The words next to "shape and cut" (round brilliant, round full, tapered baguette) are all terms for shape only. Cut information, describing the stone's precise geometric proportions (table %, crown angle, pavilion %--highlighted on ACORD 18), is simply not given. Cut is one of the "4 Cs" of gems, along with color, clarity and carat weight. In diamonds, cut accounts for fully half the gem's value. A reliable valuation cannot be made without this information.

A little fudging appears in the description of clarity as SI3 ("slightly imperfect-3") There is no such designation in standard GIA grading. This grade actually translates to I1 ("imperfect-1"), which means inclusions are visible to the naked eye.

Appraisal 2

|

|

Appraisal 2 |

Appraisal 2 |

This succinct appraisal leaves out crucial cut and mounting information.

Notice also the paragraph that follows the appraiser's signature. It begins by certifying the truth and correctness of the appraisal, but then undercuts that assurance by stating "We assume no liability with respect to any action that may be taken on the basis of this appraisal." It may as well say: Don't base your claim settlement on this appraisal and valuation.

A professional appraiser should, in fact, stand behind his word and expertise. For a more trustworthy warrantee of truth, see the paragraph above the appraiser's signature on the ACORD 78/79 appraisal.

Appraisal 3

|

|

Appraisal 3 |

Appraisal 3 |

In addition to all the missing information highlighted on ACORD 18, this one isn't even called an appraisal — and the title says it all. The no-liability clause, above the appraiser's signature, emphasizes again that this is not really an important document. It is, after all, just for insurance.

Appraisal 4

|

|

Appraisal 4 |

Appraisal 4 |

This is a so-called "narrative" appraisal, where all information is packed into a dense paragraph. ACORD 18 shows that information is missing on cut, setting and mounting.

Since this jewelry was the subject of a damage claim, rather than a total loss, other appraisal problems became apparent. The appraisal describes the emerald as yellow green, but examination of the damaged stone showed it to be bluish green. In addition, tone and saturation were omitted. These discrepancies are not trivial. The major determinant for an emerald's value is its color, and the descriptive language for color stones is standardized and quite precise.

Based on the replacement cost submitted by the original seller/ appraiser, the insurer settled the claim for $49,000. JCRS, consulted afterwards to deal with the salvage, found that the emerald could have been replaced for $8,279.

The original appraisal was grossly inflated. In settling the claim the adjuster made two mistakes: 1) he accepted the appraisal at face value, and 2) he accepted the selling jeweler's cost of replacement. If, instead, he had consulted a disinterested jewelry professional to verify valuation before settling the claim, he could have avoided the $40,000 overpayment.

Appraisal 5

|

|

Appraisal 5 |

Appraisal 5 |

This is a formal and impressive-looking document, patterned after the Diamond

Reports produced by such respected labs as the Gemological Institute of America.

This, however, is NOT from a respected lab. It leaves out the same crucial

information omitted on handwritten appraisals from mom-and-pop jewelers.

To cap it off, the valuation is also grossly inflated. Appraisals with inflated valuations are often used as sales tools, to convince purchasers they are getting bargains.

Summary

- NONE of these appraisals has complete information on cut.

- NONE of these appraisals has complete information on mounting.

- NONE gives the manufacturer, style number, or workmanship, and one even omits weight.

- NONE describes the setting.

- And only one of them was prepared by a graduate gemologist.

Unfortunately, these inadequacies are typical. A decade ago JCRS completed a survey of appraisals from 21 insurance companies. Only one percent of the appraisals studied mentioned cut, the single quality most important in valuing diamonds. Only 11 percent gave manufacturer; just 6 percent listed manufacturing technique. Four fifths of the appraisals were prepared by jewelers with no formal gemological training.

Today, insurers are seeing appraisals with exactly the same problems. What has changed in ten years?

What's changed is that ACORD has adopted standards for jewelry appraisals. Insurers need not continue accepting any inadequate appraisal a jeweler puts out.

- ACORD 78/79, Jewelry Appraisal, clearly lays out what detailed information the insurer needs. It requires also that the appraiser be a graduate gemologist and a Certified Insurance Appraiser.

- ACORD 805, Detailed Sales Receipt, sets the standard for documenting sales. It can be filled out by any selling jeweler (regardless of training).

- ACORD 18, Jewelry Appraisal & Claim Evaluation, can be used by insurers to score any appraisal for necessary information. Software makes the results apparent by highlighting any missing information.

There are also Jewelry Insurance Workshops to train agents, underwriters and adjusters in how to analyze jewelry appraisals, avoid fraud and reduce settlement costs.

FOR UNDERWRITERS & AGENTS

Recommend that your policyholders submit ACORD 78/79 appraisals. This guarantees that the jewelry was inspected by a graduate gemologist who is a Certified Insurance Appraiser™ and that all necessary descriptive information appears on the appraisal.

Your second preference should be ACORD 805, a Detailed Sales Receipt.

Insist on a second appraisal for all jewelry valued at $25,000 or more. This in itself lessens the risk of being taken in by an inflated appraisal supplied by the seller. If the first appraisal was not on ACORD 78/79, this one should be.

FOR ADJUSTERS

If you are not working with an ACORD 78/79 appraisal or an ACORD 805 Sales Receipt, use ACORD 18 to analyze the data you have from the existing appraisal and other documents.

Always have damaged jewelry examined by an impartial jeweler — preferably an expert working on your behalf — to verify truth of the appraisal descriptions and valuation.

Rely on your own jewelry expert to estimate cost of repair or replacement. Do not blindly accept the bid of the selling jeweler.

©2000-2025, JCRS Inland Marine Solutions, Inc. All Rights Reserved. www.jcrs.com

Subscribe to Jewelry Insurance Issues